The battle between Chinese and American chips has been foreshadowed. What areas are China's opportunities and challenges focused on?

In January 2017, less than two weeks after Trump was sworn in, the White House issued a report “Ensuring Long-Term US Leadership in Semiconductorsâ€, citing the United States President’s Science and Technology Advisory Committee. .

The report elaborated on the committee's viewpoints on the status quo of China-US semiconductor development, the threats China has brought to the United States, and specific recommendations. The report pointed out that China’s support to the semiconductor industry will pose a threat to the United States; from this, we can also fully understand the strategic positioning and strategic choice of the United States for the integrated circuit industry.

General

Semiconductor is an important part of modern life. It has also opened up many new business models and industries. It is also an important guarantee for the United States' defense system and military strength. Integrated circuits are the country's strategic, basic, and leading industries.

This report elaborates and recommends three key strategies to maintain the lead of U.S. Semiconductor:

(1) Suppression of innovation in China's semiconductor industry (Americans explicitly stated that the introduction of semiconductor core technologies from the United States, such as market-for-technology, do not even think about it);

(2) To improve the business environment of US-based semiconductor companies (even if Americans want to change the environment for an industry, China's financial and taxation departments say that they can not develop special policies for the specific industry of integrated circuits.)

(3) Promoting semiconductor innovation transfer in the next few decades (over 95% of China's central government and local governments have invested in catching up with mainstream American technologies, and the power spent on future technologies is still too little!).

The government, industry and academia need to work together (China's cross-border cooperation is still pleasant).

I. Outline

Historically, the global semiconductor market has never been a completely competitive market. (This sentence is the crowning touch in the full text. The United States, as the world’s leading semiconductor in the world, is still emphasizing this point; we, as a chase-breaker for making 1-2 generations behind, some equipment materials, and even no R&D capabilities, should especially Highlight the national property of the integrated circuit, the guiding nature of the government, make a determination, spend 10-20 years, concentrate on investment, and become bigger and stronger.)

In the process of innovation, the U.S. government should also try its best to stop China’s destruction and influence. We give three suggestions:

(1) The United States should have talks with China and understand China's true intentions (a sound industrial system only) by joining the alliance. (This alliance should not encourage China to join the alliance, but the US and Europe and the United States form an alliance to contain China. ) Consolidate internal investment security and export controls, and limit some of China's certain violations of international agreements (it is even more difficult to purchase US semiconductor technology in the future). The United States also needs to adjust its homeland security related agreements to prevent possible security threats from China. (The United States does not understand that the more he confines semiconductor technology, the more he forces China to develop semiconductor technology. Similarly, the US says To prevent China's security threats, the US threat felt by China under this stance is at least equal;)

(2) We believe that a competitive local industry is a guarantee of innovation and safety. We recommend that the government formulate strategies to attract highly talented researchers to invest in related R&D. And help with policies, funding, and taxation (note that the Americans explicitly proposed the concepts of capital and taxation. Funds are subsidies, the United States generally appears in the form of commissioned contracts; taxes are very powerful, and are opened for the semiconductor industry. Green tax revenue, China's fiscal and taxation departments should learn!);

Second, challenges and opportunities

Historically, the U.S. government’s support for R&D has been fundamental to promoting semiconductor innovation. But once the industry is “emptyâ€, there is no value in these supports (this is in line with the return of high-end manufacturing advocated by the United States in recent years).

If the U.S. government maintains its competitive advantage by isolating its industry from its foreign competitors, innovation will be hit and the U.S. industrial competitiveness and economy will be affected. (Think tanks still do not recommend simple blocking of Chinese semiconductor competitors. After all, The bans are mutual, damaging to American counterparts' market expansion and technological innovation capabilities.

In order to maintain its national defense advantage, the military needs to have semiconductor technology that some potential rivals do not own. Official buyers, including the military, also need to mitigate the risks posed by the semiconductor supply chain. They also need to address the risks posed by integrity and availability (China needs a sound industrial system).

A strong local industry can ease these security threats, but it is not a long-term solution. Placing key devices in the United States to design, manufacture, and manufacture can reduce the risks facing US semiconductors, but we can't do this easily (manufacturing returns, it's hard). Therefore, we need to explore other methods to ensure safety regardless of where the semiconductor products come from. If the United States wants to ensure safety through simple restrictions on companies that sell semiconductor products to the United States, this will lead to market segmentation and competition weakening, and eventually lead to slow innovation; this will reduce the likelihood of the United States acquiring advanced chips (here are some Layer meaning: First, think tanks still admit that foreign suppliers including China are likely to have more advanced chips than US companies; Second, they hope to allow overseas chips to be sold in the United States through a security review; The simple blockade of Chinese chip suppliers is not conducive to US innovation.

Attachment: Status Quo of Semiconductor Industry in the United States

In the past two decades, sales of semiconductor companies in the United States accounted for more than half of the world's total, and no mainland Chinese companies have entered the top twenty.

The United States still monopolizes important areas of semiconductors. The United States also has most of the world's IC design companies and Fab factories, which account for 80% of the semiconductor market. In the area of ​​integrated circuits, the United States has unparalleled advantages in terms of logic and simulation. In particular, the U.S. has world-leading advantages in high-end microprocessors and communication chips used in smart phones and devices. In addition, the United States is a well-deserved brother in routers, the Internet, and fixed-line telephone exchange network devices. The world’s largest IDM (Intel), the top three fabless companies and the world’s top three EDA design companies are all in the United States. In addition, from the point of view of revenue, the two major headquarters of the three major equipment manufacturers are also located in the United States.

Third, the challenges of evolution

(1) Technology and Market

Moore's Law doubles the number of integrated devices every 18-24 months, and at the same time reduces chip costs. Continuing this law now faces major challenges. The current cycle has been extended to 30 months (the pace of technological renewal slows down, and it is the United States that is worried about one of the main reasons why China catches up faster).

Semiconductors also need to face the highly concentrated challenges of the industry. The world’s top five semiconductor companies account for 40% of the world’s sales, an increase of 8 percentage points from 32% in 2006. The pressure of cost now is pushing semiconductor companies to get warm. For example, in order to meet the technical challenges of speed and miniaturization, the cost of the US-based Fab spent on advanced logic technology is as high as US$12 billion, and five years ago, the corresponding cost was US$5 billion (scale investment).

(2) Impact of China's semiconductor strategy

The slow pace of innovation, the shift in the market, and the concentration of industries will bring them enormous challenges. But this is not as great as the impact of China.

China's pursuit of semiconductor technology is far behind the United States. This is undoubtedly true (think think tanks are accurate and there is no deliberate fictional direct threat). China's advanced logic manufacturing technology is much less than that of the United States, Taiwan and other advanced semiconductor players. There are many semiconductor fabs in China, but they are 1 to 1.5 generations behind the current mainstream process (China's best factory is 1-1.5 generations behind the United States, and most factories are more than two generations older than the mainstream). In terms of storage, although China is investing heavily, it is clear that China currently does not have local-related production enterprises. Now China's domestic production of advanced storage is the output of foreign companies in China’s investment enterprises (the Yangtze River is Storage has not yet been put into production. The mass production is Wuxi Hynix.

Now that China has adopted non-market methods and uses various strategies and strategies, it expects to gain a global leading position in the design and manufacturing of semiconductors. It seems that this can be done with force. However, policy documents still seldom mention the global leader. Look at this. The Americans who make the semiconductors are very nervous; it's like a small tiger cub is just weaning and he has to be everywhere to say that he wants to be the king of the forest. What do you think of the king of the tiger? With the increase in the consumption of semiconductor products in China (the US think tank cannot ignore China's huge semiconductor market), this has made the challenges faced by the semiconductor industry even more complicated.

China lacks the first echelon of semiconductor equipment companies, but there is a second-tier equipment company in Shanghai, that is AMEC (China Microelectronics, entering the second echelon has been difficult, should be proud of; the next step is to follow the practice of Europe and the United States, widely After the merger, do large-scale).

In this environment, China Semiconductor can only improve its competitiveness by acquiring advanced semiconductor companies or some of its departments overseas including the United States, Japan, Europe, South Korea, and Taiwan. And China’s investment in this area is also significantly increased (I feel that China’s fragmentation is now obvious, sometimes mergers and acquisitions, to make a big profit on buying back; lack of government to invest in large companies around the leading companies Government funds acquisitions).

It now appears that the most prominent area of ​​China's semiconductor performance is Fabless. But frankly speaking, there is still a big gap between these Fabless in China and foreign advanced colleagues. From the current perspective, most of the Chinese fabless are aimed at the low-end and mid-range markets.

Out of consideration for economic and homeland security, the Chinese government has publicly declared that it will create a more advanced and complete semiconductor industrial chain than it is now, in order to reduce its dependence on foreign countries. After a decade of failed semiconductor attempts, China promulgated the "IC Promotion Program" in 2014 to promote the development of China's semiconductor industry. The program includes revenue requirements and technical goals. This program has also won the support of many senior Chinese leaders, including President Xi Jinping. One of the main goals is that China hopes to increase the level of its semiconductor industrial chain to the world's top camp by 2030.

China's semiconductor strategy relies on its huge financial support. This is an investment that includes state funds and private equity, with a total amount of up to 150 billion U.S. dollars and a ten-year cycle. Whereas the acquisition of technology, China hopes to obtain through the investment and acquisition of advanced enterprises. The U.S. $23 billion in mergers and acquisitions over the past five years is a comparison of its scale. Many Chinese investment agencies now follow the government's guidelines and have started crazy mergers and acquisitions.

Looking at China's semiconductor construction strategy, it is mainly composed of two aspects: First, subsidy; on the other hand, it is a zero-sum game (zero sum is not a strategy; it is a result of international semiconductor competition caused by the Chinese strategy of the US think tank).

Fourth, coping strategies

In order to meet these challenges, US policy makers should follow the following six guidelines:

1. In order to win, you must run faster

2. Focus on advanced semiconductor technology research and development

3, create their own advantages, create a good environment

4. Estimate China's Response to U.S. Strategy

5. Do not oppose China's progress conditionally. The U.S. government needs to identify those special semiconductor technologies and companies, protect them, and reject them to avoid possible security threats (this applies equally to China, not only semiconductors, but should be broader, as in every field. The first place should not be merged by foreign capital; look at today's dozens of daily necessities, which are all eliminated after foreign brands bought the Chinese first and second brands. Is this not a security threat?).

6. Implementation of trade and investment regulations

V. Plans Affecting China

The United States has many ways to limit China's actions. This includes formal and informal trade and investment regulations, as well as similar CFIUS unilateral review tools based on homeland security considerations. It seems that these restrictions are still very significant. The U.S. government needs to continue to study these policies and avoid possible threats to the country’s economy and security.

(1) Promote the transparency of global advanced technology

Ideally, the world should create a fair and market-oriented environment for the semiconductor industry. Of course, for the sake of homeland security, some exceptions are allowed. (If you believe that books are better than no books, listen to Americans better than doing nothing. In the past few years, China just launched the independent innovation product procurement method and was stopped by the Americans. We A little naive; stop will give us market status treatment?). However, it seems a bit difficult to reach an agreement with China. Therefore, the U.S. government needs to promote China’s transparency in its advanced semiconductor technology strategy.

(2) Obstruction of China's relevant policies with national security when necessary

The United States should use defense security as a starting point for making relevant decisions. In some areas, China should not give any possibility of negotiation. As long as China still adheres to their unreasonable policies, the United States should and should continue to implement these strategies. For example, China's so-called "safety and controllability" in the field of information technology should be used as a reference for the development of the United States' strategy. (The United States calls for the control of national defense security and opposes China's pursuit of safety, control, and odd talk). The United States should limit China’s acquisition of U.S. companies and limit exports. (From the safe and controllable public opinion, it can be seen that the U.S. can never lift the blockade against China until he was defeated).

(3) Join hands with allies to strengthen global export control and internal investment security

The United States is committed to promoting physical export control and investment security. The United States should also work with the alliance to develop rules of relevance and extend it to other markets. In the era of globalization of semiconductors, unilateral agreements are ineffective, even though the United States leads semiconductors globally and holds the unilateral agreement (this is the same as the United States fighting in the Middle East, although the United States can easily crush any opponent in the Middle East, but We must bring together other younger brothers so that the United States can be truly safe. After the gang fights, the law does not condemn people.

Sixth, create a better industrial environment in the United States

Staff reserves, strengthen general scientific research, and promote tax reform. This is what the industry has been calling for. Including:

(1) Guarantee the output of talent

Investment will occur where talent is found. The United States should continue to promote the cultivation of local talent and attract geniuses from around the world.

Thanks to the efforts of the industry, the United States does a good job in the talent pool. The sustained investment in STEM, the impact on the US industry is obvious (STEM, science, technology, engineering, mathematics, have to listen to the views of colleges and universities, these four aspects of our semiconductor talent layout intact).

The United States also needs to attract geniuses from around the world. The United States needs to use various kinds of offers to attract various high-end talents (the same applies to China).

(2) Investment in Advanced Technology

Investment in advanced fields is the basis for maintaining the competitiveness of the semiconductor industry. For example, the recent research on wide bandgap semiconductors is supported by government-led basic research, but it has now been widely spread and applied to include electric vehicle charging and solar energy. Therefore, the investment in advanced science and technology is the United States must adhere to the principle (can dissect, the United States by what means to support wide-band gap semiconductor research and carbon nanotube research?).

In the semiconductor field, 20% of revenue is invested in R&D, and this money is used in competitors' research and product development. The government’s investment in advanced technology can accelerate innovation and ultimately return to the government. For example, the government's research on carbon nanotubes does not specify in which direction, but the industry will apply it to advanced semiconductors and other technical fields.

(Advanced technology investment is too important. There is currently no obvious gradient in the country. This is a defect. The advanced technology proposed by the US think tank here is the third category. The three types of technologies are classified as follows: Currently selling for 1-2 years, stocking a generation of products for sales within 2-5 years, and proactively laying out a generation of technology to deal with possible revolutionary changes in the industry.China's semiconductor industry is currently focusing more on catching up, the first being the main one; The resources invested by the government can be used more in the third category. Once the company has no spare cash, it can be used to worry about it. Second, if there is a breakthrough, it is subversive.)

(3) Promote tax reform

This can ignite the passion of entrepreneurs (we should allow qualified regions to learn from semiconductors developed in Taiwan and pilot relevant taxation policies, such as the supervision of integrated circuit industry chains).

(4) Promote the construction of advanced facilities

This can guarantee the ancestors of the study (Shanghai, Hefei, Beijing, some advanced facilities, but did not hear that advanced facilities are widely used in semiconductor materials and process research, is a lack of scientific research in this area? Or the country has not systematically considered this direction?).

7. In order to maintain the leading position in the United States, it is necessary to create a "leaping frog" strategy.

(In this paragraph, the U.S. think tanks mainly talk about how to lay out the second and third types of technologies that I mentioned earlier; the first U.S. government does not have to worry about, and the companies themselves will handle them.)

If the United States confines its vision to creating a cheaper and more convenient semiconductor industry and is indifferent to the destructive rise of China, then the United States will not maintain its leading position in semiconductors. Therefore, in order to maintain the leading position of US semiconductors, we need to formulate an advanced strategy. In order to strengthen the competitiveness and innovation of semiconductors, we propose to focus on the following four principles: (1) Adopt application-driven methods to lead innovation. (2) Take a decade as a stage. (3) Compensation for investments in vulnerable industries. Similar fields such as artificial intelligence, big data analysis, and self-driving automotive systems (second type of technology), because of promising prospects and quick feedback, the investments that attract are natural; but similar materials science, advanced manufacturing, and space technology To return the basic disciplines with longer periods (third-class technologies), we need to favor them because these are the basics of all industries. (4) Reduce design costs. Like the 1980s that promoted the development of EDA to reduce costs, the U.S. government should promote the development of more new technologies and reduce the cost of design (this highlights the importance of chip design tools, and it is even more super-short at home).

VIII. What areas are the opportunities and challenges focused on?

For a long time, U.S. Semiconductor has not been faced with such a severe challenge. This time, industry, academia, and the government are needed to meet this challenge. In the foreseeable future, we believe that opportunities and challenges will be faced in the following areas (so-called opportunities and challenges, that is, American companies must first come up with, that is, opportunities; Chinese companies must first come up with it, that is, everyone's challenges. Come on!):

(1) Architecture

(a) von Neumann architecture. Multi-core processors will become demand in the future, which will promote the transformation of the von Neumann architecture (second technology).

(b) Quantum. Quantum computing may revolutionize computing power. There are also several different quantum architectures that need to be measured and selected (third-class technologies).

(c) Neuromorphic calculations. This is also a trend in the future (third technology)

(d) Simulation calculations. Analog computing will precede digital computing revolutions and will solve problems that some numbers have not yet solved. However, in practical applications, digital computing suppresses the analog calculation. (The third type of technology)

(e) Special-purpose architecture. FPGAs, GPUs, deep learning/machine learning accelerators, edge calculations, are some of the potential directions for development (secondary technologies).

(f) Approximate calculations. Can solve multimedia processing, machine learning, signal processing problems.

(2) Calculation form

Embedded systems, personal and portable systems, and very large-scale systems can all change in the future.

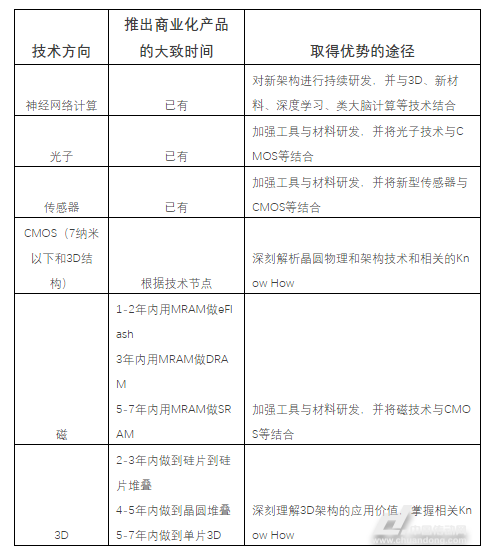

(3) Technology that may make progress in the next decade

220W Medical Power Supply,220W Medical Device Power Supply,220W Medical Power Adapter,220W Rade Power Supplies

Shenzhen Longxc Power Supply Co., Ltd , https://www.longxcpower.com